As financial services learn more about us and use big data to help form a more nuanced picture of who we are, there is growing concern that this shifts the balance of power towards financial providers and away from consumers.

The world of finance traditionally moves slower in its adoption of tech innovations and reaction to social shifts for reasons including heavy regulation, concern for security and customer inertia. While positioning themselves as neutral and impartial, these institutions hold incredible amounts of personal data on customers. This has created an emerging debate about who actually holds the power.

It is fascinating to see how decision-making is playing out in the context of money, particularly in an industry characterised by confusing jargon, endless small print and undifferentiated offers that often work against how we naturally make decisions.

With the burden of knowledge, can financial services remain impartial?

Financial services have been a cornerstone of the British economy for hundreds of years and have weathered many political and social shifts; from royal intervention and industrial revolution to world wars and global recessions. This enduring nature has been built on a position of neutrality and consistency, where the financial industry is a force of balance responding to the ebbs and flows of the market without shaping them itself. Typified in Lloyd’s “By Your Side” advert, this narrative was echoed post-referendum to reassure customers around the uncertainty caused by Brexit.

Current worries focus on businesses using big data to sort through the incredible depth of information and coerce customers into the most profitable outcomes. In an attempt to rebalance this relationship, digital tools are emerging to help alleviate the pressure placed on consumers to make the right decision. The most direct version of these tools are the auto-switching services, which have emerged in low engagement categories like energy and credit cards, where brands are trying to take control of these decisions on behalf of customers.

Current worries focus on businesses using big data to sort through the incredible depth of information and coerce customers into the most profitable outcomes. In an attempt to rebalance this relationship, digital tools are emerging to help alleviate the pressure placed on consumers to make the right decision. The most direct version of these tools are the auto-switching services, which have emerged in low engagement categories like energy and credit cards, where brands are trying to take control of these decisions on behalf of customers.

Consumers who surrender their responsibility of decision-making feel like they are unable (or unwilling) to make informed decisions themselves. This addresses the short-term symptom of stress, confusion and provides a definitive answer (even if it isn’t the best one) which is valuable in the current landscape, but not ideal. Beyond issues of trust, these services are a symptom of an industry which has made it difficult to make clear, informed and accessible decisions for ourselves.

Consumers who surrender their responsibility of decision-making feel like they are unable (or unwilling) to make informed decisions themselves. This addresses the short-term symptom of stress, confusion and provides a definitive answer (even if it isn’t the best one) which is valuable in the current landscape, but not ideal. Beyond issues of trust, these services are a symptom of an industry which has made it difficult to make clear, informed and accessible decisions for ourselves.

Digital tools should help us make informed decisions

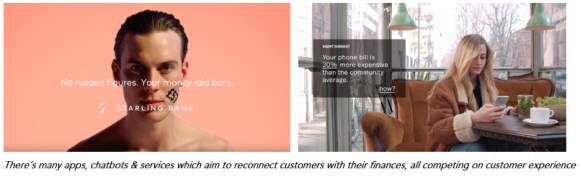

The core proposition behind many new fintechs is to democratise the financial tools which help businesses analyse their customers. With a strong focus on customer experience, there are various ways they pitch this information back to customers in a human and relatable manner – devoid of all the industry terms that can leave us confused. Current accounts such as Starling and N26 aim to empower the individual by being totally and immediately transparent, providing an in-depth analysis of an individual’s financial world, to help them make the best choices about their spending. Other savings tools such as Oval, use social comparisons to put our individual data into context of our peers, helping to cut through generic recommendations about ‘saving money’ and focus on specific aspects of where we’re overspending.

Ultimately, the responsibility of the decisions we make should rest on our shoulders. The internet has armed us with information and empowered us to make our own decisions. Independent, savvy consumers still want to do this but are overwhelmed with how the landscape has evolved. Rather than regressing, brands should seek to help us navigate this and empower us to make the right kind of decisions, without being overbearing.

Ultimately, the responsibility of the decisions we make should rest on our shoulders. The internet has armed us with information and empowered us to make our own decisions. Independent, savvy consumers still want to do this but are overwhelmed with how the landscape has evolved. Rather than regressing, brands should seek to help us navigate this and empower us to make the right kind of decisions, without being overbearing.

Businesses who readdress the balance of power and provide an environment where customers reengage with their finances in a positive way, will be more trusted to influence how customers make many of their financial decisions in the future.

Businesses who readdress the balance of power and provide an environment where customers reengage with their finances in a positive way, will be more trusted to influence how customers make many of their financial decisions in the future.